UK construction companies report business activity and employment levels both expanding at a strong pace. There are also signs that strains on raw material availability have started to subside, as highlighted by the slowest deterioration in vendor performance for just over three years.

Survey respondents noted that rising levels of supplier capacity, alongside lower fuel and energy costs, had helped restrain overall input price inflation in August.

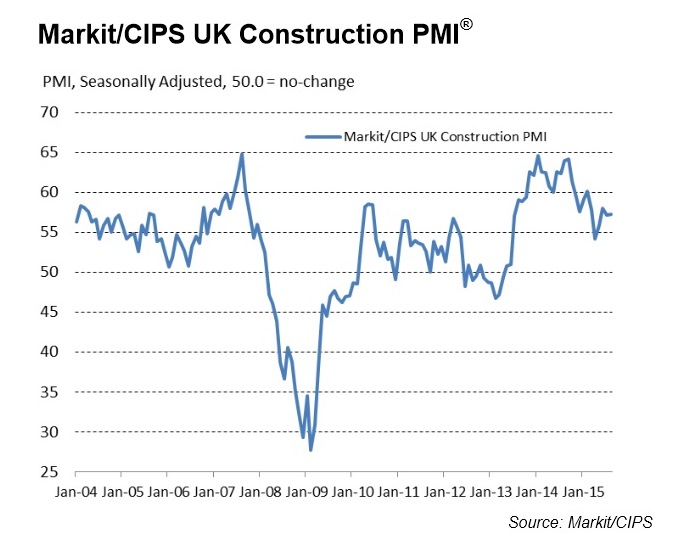

The headline seasonally adjusted Markit/CIPS UK Construction Purchasing Managers’ Index (PMI) registered 57.3 in August, up from 57.1 in July and well above the neutral 50.0 threshold.

Higher levels of business activity have been recorded in each month since May 2013, which represents the longest period of sustained growth for seven-and-a-half years. That said, the index continued to signal a softer growth path than that recorded throughout 2014.

Of the three broad sectors monitored by the survey, the fastest pace of expansion was in residential construction. Growth of commercial work also accelerated since the previous month, reaching its strongest since March. Survey respondents widely linked the latest upturn to improving economic conditions and strong demand from private sector clients. Meanwhile, civil engineering was the weakest performing broad area of activity, with the latest rise in output the slowest for three months.

August data pointed to a solid expansion in new business intakes across the UK construction sector, but the rate of growth eased to its least marked since May. Survey respondents were generally upbeat, however, about underlying market conditions and the number of opportunities to tender. Some firms simply noted that capacity constraints at their business units had held back their ability to take on new work and, in some cases, allowed them to become more selective about development opportunities.

Looking ahead, more than half of the survey panel (53%) anticipate a rise in business activity over the next 12 months, while only 5% forecast a reduction.

Although the degree of optimism remained below June’s 11-year high, the latest reading was comfortably above the long-run survey average.

Increased workloads and impending new project starts contributed to a robust rate of job creation in August. The current period of staff hiring now stretches to 27 successive months, which is the longest recorded by the survey for just over nine years. Subcontractor usage also picked up again, with the pace of expansion the fastest since February.

The latest survey highlighted that subcontractor charges rose sharply, but the rate of inflation slipped to its lowest since April 2014. Meanwhile, lower oil-related prices contributed to the weakest overall rate of cost inflation for four months in August.

Markit senior economist Tim Moore said: “UK construction companies remained on a reasonably strong growth footing in August, helped by a sustained recovery in both residential and commercial building activity. Meanwhile, there was another loss of momentum for civil engineering, which brought output growth within this sub-sector further below the multi-year highs seen in 2014.

“The construction sector maintained its position as a strong engine of job creation in August, as permanent staff numbers and subcontractor demand both picked up over the month. However, the surge in construction workloads over the past two-and-a-half years has created substantial skill shortages across the sector, with survey respondents reporting ongoing staff recruitment difficulties this summer.

“There was some encouraging news in terms of construction materials availability, as firms reported the lowest pressure on delivery times for over three years, helped by rising inventories and a rebound in supplier capacity.”

Got a story? Email news@theconstructionindex.co.uk