Recovery is needed after the Office for National Statistics (ONS) simultaneously reported a 14.1% fall in new orders for 2011.

According to the ONS, new construction orders fell a further 2.5% in the fourth quarter of 2011 compared to the third quarter.

The total volume of all new construction orders in 2011 was 14.1% lower than 2010 and at the lowest level since 1980.

The biggest falling segment in the fourth quarter was public housing, down 26% quarter on quarter.

For the year as a whole, the largest decreases were in the segments of other public new work (34.7%) and public new housing (28.3%) - constant (2005) prices, seasonally adjusted basis.

If it wasn’t for Crossrail’s huge contract awards, the decline would have been much greater. Thanks to the rail and power sectors, there was a 41.6% rise in new orders for infrastructure work in the fourth quarter, the strongest rising segment.

Civil Engineering Contractors Association director of external affairs Alasdair Reisner cautioned that some aspects of infrastructure workload were in decline. "For example, activity in the roads sector in Q4 2011 is at almost half the average level seen in the past three years. For many contractors, including those serving local communities and specialist markets, the outlook for orders remains extremely poor."

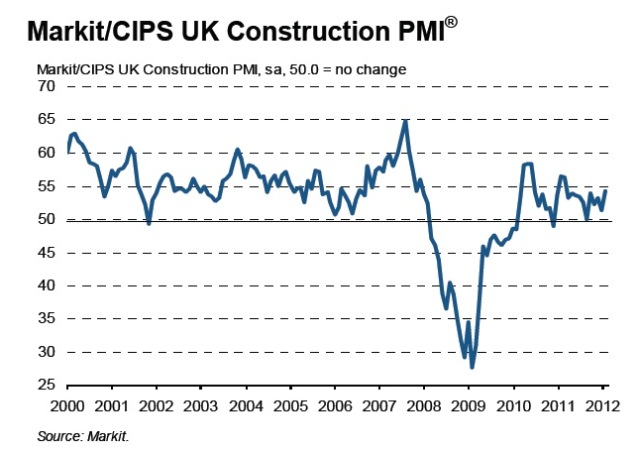

However, there appears to have been improvement across the construction industry in February, with the seasonally adjusted Markit/CIPS Construction Purchasing Managers’ Index (PMI) posting 54.3 – the 14thconsecutive month of growth. Up from 51.4 in January, the index posted its highest reading since March 2011. Any reading over 50 indicates growth. February’s data pointed to a solid expansion of construction sector output that was in line with the series average.

The stronger expansion in activity was supported by a sharp rise in new work intakes. However, accelerated growth of both new business and output were insufficient to prevent a fall in employment. Meanwhile, a fourth successive improvement in confidence was indicated.

February data signalled a reduction of employment, despite expansions of both activity and new business. Job cuts due to reorganisations at some companies outweighed hiring activity to accommodate higher workflows at others. Nonetheless, the decrease in staffing levels was only marginal. Similarly, subcontractor usage also fell in February at a marginal pace.

Markit economist Sarah Bingham said: “The slowdown in UK construction sector output growth recorded in January was reversed in February, with a solid increase in activity indicated. This was despite potential headwinds caused by poor weather conditions. The rise in output was supported by a stronger commercial expansion. Residential construction and civil engineering activity also increased, rebounding from contractions last month.

“Perhaps more encouraging was the sharp increase in new business received, which should keep firms busy in the coming months. Reports of rising tender opportunities and greater visibility over potential new work flows also helped to boost confidence about the year ahead, which rose to a nine-month high.

“The improved performance of the construction sector adds to other positive data released on the UK economy. However, it remains to be seen whether GDP growth for the first quarter will be recorded and, if it is, any expansion is likely to be only modest as general economic conditions remain fragile.”

Quantity surveyor EC Harris research head Simon Rawlinson said of the PMI data: “Thefigures announced this morning are very positive indicating confidence is rising and the pipeline is building across housing, commercial and civil engineering. An index figure of 54.3 is the strongest since March 2012 and this positive sign aligns with other ‘green shoots’ indicators suggesting an improvement in business sentiment. However, the PMI index does not appear to be picking up the significant downturn in public sector work reported in output and new orders data.

“Encouragingly for industry, the level of input inflation reported is at the lowest level for two years – this will reduce pressure on the supply chain, when in our opinion there is limited opportunity for price inflation over the next 12 months.”

On the ONS new order numbers, he added: “A stable headline figure for new orders masks the continuing decline of the public sector as a client and lower than expected level of activity in the commercial sector. Orders in real terms were £7 billion (14%) down on volumes recorded in 2010. Due to the sampling method, this does not necessarily point to a corresponding reduction in output, but the signs are not positive for 2012.

“The only sector to have increased overall orders during full year 2011 is private housing (6%) pointing to steady recovery which should get a further boost in March 2012 with the introduction of the NewBuy initiative. By contrast, total public sector non-housing orders in 2011 fell by 35% compared to 2010 although this has barely filtered through to output yet."

He concluded: “Overall sparkling infrastructure figures mask a significant decline in other sources of workload. Resource pressure in the infrastructure sectors could be building whilst workload for the squeezed middle in public sector and commercial worlds face further challenges. House building looks well set to be a source of growth during 2012 which may compensate for disappointment in the commercial sector.“

Got a story? Email news@theconstructionindex.co.uk