However, purchasing activity and employment both continued to decline during the month according to the latest Ulster Bank Construction Purchasing Managers’ Index (PMI ).

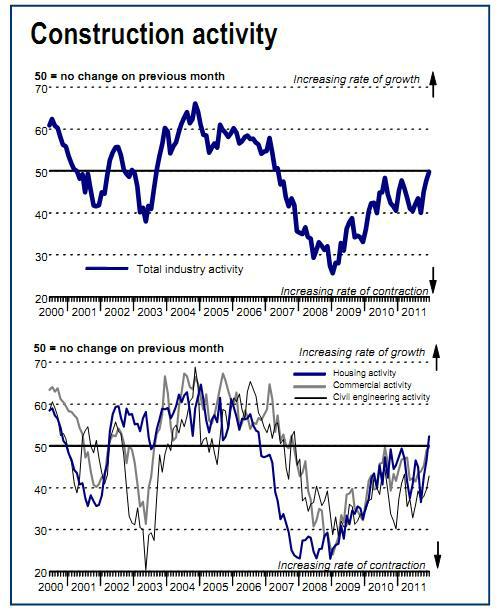

The seasonally adjusted, which is designed to track changes in total construction activity, rose to 49.9 in December from 47.7, to signal only a negligible reduction in activity during the month. The latest reading was the highest since May 2007. Although a number of firms reported that business conditions remained fragile, others indicated that new order growth had acted to boost activity.

“There were further signs that the Irish construction sector may be approaching a point of stabilisation in the latest reading of the Ulster Bank Construction Purchasing Managers Index (PMI),” said Ulster Bank chief economist Republic of Ireland Simon Barry. “The December survey featured several encouraging developments including that the overall PMI rose to its highest level in over four and a half years. At 49.9, the PMI is just a fraction below the expansion-contraction threshold level of 50 indicating that the pace of decline in construction activity last month was negligible.”

The results point to a slight increase in housing activity last month – the first time the survey has pointed to a rise since October 2006 – while the rate of decline in commercial activity eased for the fifth month in a row to just a fraction below the 50 level. “As has been the case for most of the past two years, activity in Civil Engineering continues to underperform quite markedly and, unlike the other two sub-sectors, is continuing to contract at a sharp pace,” he said.

“Also offering encouragement was a rise in the new orders index to back above 50 for the second time in three months, as some firms reported higher levels of new business,” he added. “Our overall take on these latest results is that they offer some heartening evidence that, after an extraordinarily severe downturn which has lasted over four and a half years, the Irish construction sector looks to be in the early stages of a bottoming out process. It would be wrong to characterise the construction outlook as positive but it looks as if 2012 could be a year where some semblance of stability takes hold after the slump experienced over 2007-11.”

Housing activity rose for the first time since October 2006. Conversely, both commercial and civil engineering activity continued to fall. Activity on commercial projects decreased only marginally, while civil engineering activity declined sharply.

New orders increased for the second time in the past three months, and at a solid pace that was the sharpest since March 2007. According to respondents, there had been signs of stability in the market.

However, construction firms continued to lower employment during December, suggesting that the rise in new business was insufficient to prevent spare capacity existing within the sector. Although slower than in November, the rate of job shedding remained marked.

Irish construction firms reduced their input buying again in December. Although the rate of decline in purchasing activity eased slightly over the month, it was still solid. Respondents noted a reluctance to build inventories. In spite of the reduction in demand for inputs, suppliers’ delivery times lengthened over the month. Panellists attributed the deterioration to low stock levels at suppliers. Lead times have now lengthened in each of the past six months. The rate of input cost inflation slowed in December, and was weaker than the long-run series average. That said, input prices still increased for the twentieth month in a row.

Stabilisation in the sector and signs of improving new business contributed to optimism among firms that activity will be higher in 12 months’ time than current levels. The level of positive sentiment increased for the second consecutive month, and was the highest since August.

Got a story? Email news@theconstructionindex.co.uk