This year’s TCI Top 100 – a review of financial results filed by the end of June 2024 – reveals that aggregate turnover increased by 8.9%. On an individual basis, 78 companies grew their turnover; but pushing up profits proved harder with only 51 increasing their pre-tax profits.

Top 100 Construction Companies 2024 (click here to see full table)

Profit margins have come under pressure during the past year, with the average margin across the Top 100 falling to 1.7% compared to 2.7% among the same companies in 2023.

Among those construction companies quoted on the UK stock exchange, profitability has remained relatively stable. There are 14 public limited companies (plcs) that could be described as contractors and 10 feature in the latest Top 100 with piling specialist Keller excluded as the bulk of its turnover comes from overseas.

The five biggest quoted players – Balfour Beatty, Costain, Kier, Galliford Try and Morgan Sindall – are among the top 13 contractors by revenue and while they all might record pretty low margins, this should not be a cause for concern.

Alistair Stewart, a veteran construction analyst in the City, now with Progressive Equity Research, says: “It doesn’t matter how high or low margins are, it’s how certain those margins are. If I’m going to get 1.5% on huge turnover and I’m paid in advance and I’m certain that I’m getting that advance, that’s fantastic.”

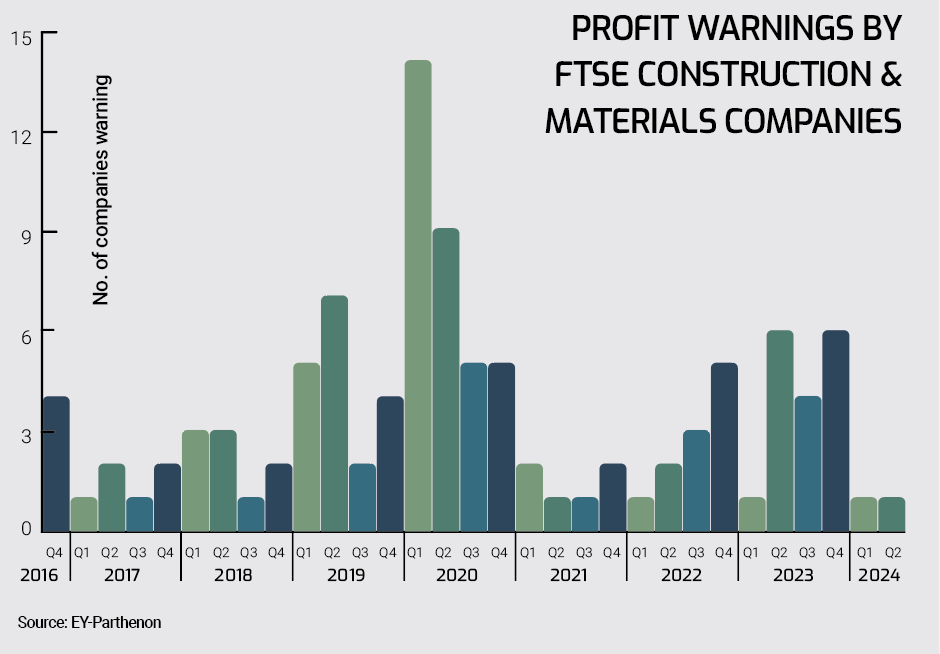

Margins may be low compared to other sectors, but according to research by EY-Parthenon, the number of companies warning the City about lower-than-expected profits in the FTSE Construction & Materials sector is at a seven-year low.

There are also a number of materials producers and product manufacturers in the FTSE Construction & Materials sector who appear to have passed on cost pressures to their customers. This is filtering down the supply chain.

EY-Parthenon warns that weaker housing activity is exacerbating stress among construction subcontractors and material suppliers that have already suffered from “unprecedented cost, labour and supply chain stresses” over the previous two years.

“Overall, construction cost inflation is lower than last year but costs remain elevated and some major contractors are asking for price cuts from their subcontractors and suppliers to offset the impact of falling demand, pushing stress down the supply

chain,” said EY-Parthenon.

A handful of main contractors continue to buckle under financial pressure, including major names such as Buckingham, which was ranked 30th in the 2023 TCI Top 100, and smaller albeit well-known outfits such as Geoffrey Osborne. But specialist contractors remain under the most pressure.

Stewart adds: “Further down the supply chain, loads of mid-ranking contractors are going bust and that’s been happening incrementally for a long time. The important thing is a strong balance sheet.”

Big specialists such as Michael Lonsdale – placed 87th in last year’s TCI Top 100 – were among the 2,500 subcontractors to go under in the 12 months to May 2024 according to data from the Insolvency Service.

Just 13 specialist contractors had sufficiently large turnover to make the latest TCI Top 100. Among the 15 biggest specialists by turnover, only nine increased turnover and 10 raised pre-tax profits, with an average margin of 2.7%.

With margins thin across the board, cash – to use the old financial adage – is king. Unlike most specialist outfits, the big main contractors typically have bigger balance sheets and have been taking protective action.

Labour and material costs might have moderated but contractors are still trimming workforces. Big names such as Bam Construction, Costain, Higgins, Lendlease, Sir Robert McAlpine and the UK arm of Skanska – all consistently in the Top 100 – have cut jobs over the past year.

Another way to tighten the belt is through deferring expenditure on items such as plant renewal, which can shore up asset valuations. In this year’s Top 100, which was compiled for TCI by financial risk analyst Company Watch, the value of the asset base has either shrunk or remained unchanged at 31 of the 100 constituent firms.

Pre-tax profits are the bottom line but operating profits are perhaps a better gauge of how a business is really functioning before any financial write-offs.

At 12.5%, Thomas Armstrong has the best operating margin among the Top 100. Only one other company in the Top 100 – Henry Boot (actually more developer than contractor) – is currently working to a double digit operating margin. In contrast, five members of the current TCI Top 100 had double digit margins a year ago.

Property work can boost margins at companies like Henry Boot and some of the other more profitable construction companies but many are just scraping by and their numbers are increasing. In this year’s Top 100, 33 companies had an operating margin of 1.0% or less. Last year, 27 of the same 100 companies were working to a margin of 1.0% or below.

This trend is reflected in Company Watch’s rating system, which gauges profit management, working capital management, liquidity and how assets are funded to produce a measure of financial health – the Company Watch H-Score. Companies are scored from 0 to 100 and any with a score of 25 or below are placed in what Company Watch calls the ‘Warning Area’.

This year’s Top 100 includes 13 companies in the Warning Area. A year ago, just 10 of those 13 companies were in the Warning Area.

So, overall, the top contractors appear to be weaker, albeit only slightly, but this comes as the industry faces up to what could be potentially monumental financial challenges.

Earlier this year, EY warned about the impact of losing ‘soft’ credit: “In sectors like construction, contingent credit – including trade credit insurance, bonding lines and payment processing advances – often acts as the invisible glue that holds a business together.

“One of the key reasons why ‘soft credit’ is underestimated is that it isn’t visible on the balance sheet, which is why it often goes unnoticed in benign credit conditions. But these aren’t benign conditions. For businesses grappling with a more difficult climate, downgraded access to contingent credit can be a significant blow — not least because other forms of credit may also be tightening.”

Since EY issued that warning, conditions have worsened with a crisis looming in the bond market where business insurance giant QBE Europe is pulling out from the supply of construction bonds for the major contractors that are essential to progressing major schemes.

Performance bonds guarantee a contractor’s obligations under its contract and protect clients against potential insolvency. Most major contracts require bond cover but providers are becoming more wary after the industry lost a number of major players, including Buckingham and Geoffrey Osborne.

With the new Labour government promising to build 1.5 million homes over the course of the next five years, many contractors are anticipating a transition from a period of project delays that forced a trimming of costs into a major upswing. This could potentially cause problems for those companies with weak balance sheets as costs will be incurred ahead of a ramping up of workloads.

Richie Pamma, assistant head of credit underwriting at insurers Allianz Trade, says: “The transition from a low-demand to a growth environment poses a risk of increased trading losses. So the next 12-18 months will pose the greatest risk during this ongoing financial crisis as companies won’t be able to absorb losses."

For the top five, with their strong balance sheets and plenty of cash in hand, the future looks secure, with a regular stream of water, electricity and housing work coming up through places on existing frameworks that do not involve cut-price tendering against rivals.

Alistair Stewart concludes: “If you have a strong balance sheet, you are capable of using the most powerful word in construction – which is “No” – and letting someone else take the work.

“The big five are getting a greater share of the work they want, which is repeat work for government clients, utilities and on housing – stuff that needs to be done at a margin of 2-3% which is decent if it’s a guaranteed margin. They are all in the right place [unlike] the rest of the market.”

This time next year, the conditions for construction look likely to be better according to most forecasts. But the position of the wider industry to meet deliver that workload may not be so sure.

Top 100 Construction Companies 2024 (click here to see full table)

Company Watch

Despite a tumultuous period for construction, most of the industry’s leading companies remain in relatively robust health, according to financial data specialist Company Watch.

Company Watch uses published financial results to analyse a company’s financial position from a number of angles including profit management, working capital management, liquidity and how assets are funded.

Each company is given a rating – the H-Score – based on how closely its accounts resemble those of companies that subsequently failed. The H-Score is displayed graphically over five years on a scale of 0 (weakest) to 100 (strongest).

Any company with a score of 25 or less is placed in what Company Watch calls the ‘warning area’.

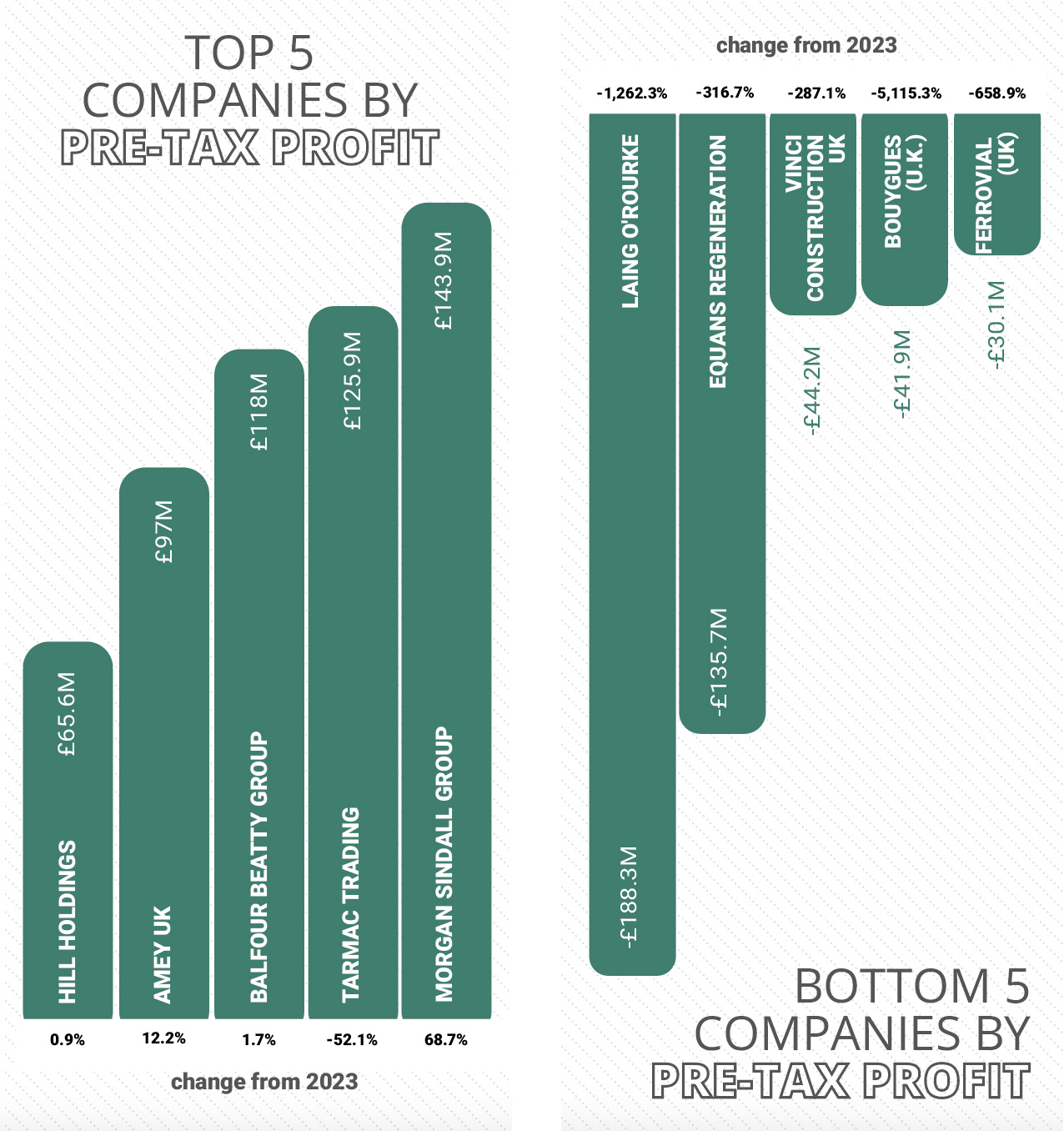

Just 13 companies in the latest TCI Top 100 are in the Company Watch warning area with Laing O’Rourke, which posted a pre-tax loss of £188.3m, rated the lowest. Cumbria-based contractor and materials group Thomas Armstrong has the highest H-Score.

Company Watch chief executive officer Craig Evans says: “In the first half of 2024, the UK construction sector faced a complex mix of challenges and opportunities. Despite inflationary pressures and interest rate hikes, the sector showed resilience with a notable decrease in firm administrations and receiverships compared to the same period in 2023.”

Company Watch also rates companies on two other measures to assess financial health.

The Probability of Distress (PoD) ratio is used for bad debt provisioning and gives the percentage probability that a distress event, such as a business failure, reconstruction or acute financial distress, will occur within one to three years. The PoD figure evaluates the H-Score in relation to the overall rate of distress across the sector, the historical rate of distress at each point on the H-Score scale and economic indicators such as growth in GDP.

A third measure of financial health from Company Watch produces different results.

The Text Score uses advanced machine learning techniques to analyse the text in financial reports of active companies to predict the probability of corporate distress. If the language or pattern of words is similar to that used by companies that have subsequently failed, the company in question could also be at risk of failing according to analysis by Company Watch.

The best-placed company on this analysis was East Anglia-based Lindum Group, while specialist contractor Enerveo is ranked lowest using this analysis. Enerveo drastically narrowed its pre-tax losses in the 2023 financial year, but is nevertheless ranked worst, below Ardmore which slumped into the red in its latest trading year.

The top five companies on this measure are all among the 13 placed in the Company Watch warning area.

Company Watch research flagged up three companies in financial distress. That trio – main contractors Buckingham and Geoffrey Osborne and specialist contractor Michael J Lonsdale – all went under and have been excluded from the TCI Top 100.

Research by Company Watch also found that, despite the relative health of most of the Top 100, another age-old financial problem dogging the construction industry appears to be getting worse: the rise of the phoenix companies. These companies – often subcontractors, that go bust and then rise out of the ashes of the old business in a slightly different guise – remain numerous and are increasing in number.

“Out of all the companies in our overall warning area, 23.99% of them are construction companies. This is a 0.4% increase year on year. Additionally, 8,090 companies have been ‘phoenixed’ from the construction sector, representing 13.3% of all known phoenixes, highlighting persistent vulnerabilities,” says Evans.

“These trends underscore ongoing concerns about financial stability within the industry. As the sector navigates these turbulent times, strategic planning and cautious optimism remain crucial."

As the industry heads – we hope – into a more positive period, the bulk of the main players look to be in reasonable financial health but the financial position of their supply chain will be vital.

Profit warnings

Profit warnings issued by companies in the construction sector have fallen to their lowest level for more than four years.

Research by consultants EY-Parthenon show just two companies in the FTSE Construction & Materials sector cautioning about lower than expected profits in the first half of this year.

Jo Robinson, head of turnaround and restructuring in UK & Ireland, said: “As we saw in 2021, after the pandemic, and 2009, after the global financial crash, a high pace of profit warnings is often followed by a steep fall if economic conditions improve and more companies meet lowered earnings expectations. But, while our data undoubtedly reflects the economic recovery, it also underscores the challenges ahead.”

Although EY-Parthenon does not identify individual firms, materials group CMO issued a profits warning in January 2024 and insulation and building materials supplier SIG followed suit in June.

While construction appears on the surface to be more resilient, the house-building sector is suffering and this could have a knock-on impact.

There were four profit warnings in Q2 2024 from companies in the FTSE Home Construction sector. This total was the third highest of any sector.

Weakness in the house-building sector has caused problems for companies in construction. At Q3 2023, EY noted that, of the 27 businesses citing a slowing of the housing market in a profit warning issued in the preceding six months, the sector most affected was Construction & Materials. In this sector, eight of the 10 profit warnings referenced the slowing housing market.

With the new Labour government looking to ease planning restrictions to meet its pledge to build 1.5 million new homes over the course of the current parliament, the longer-term outlook for the house-building sector looks better.

Construction remains at risk from cost-related issues such as labour rates and freight, while EY-Parthenon says that the sector could suffer from the impact of losing ‘soft’ credit.

In its latest update for Q2 2024, the company added: “Lenders are assigning more risk to companies in sectors like retail, construction, and real estate with elevated stress levels.”

Profit warnings in construction may have hit a record low, but with stresses in the pipeline an upturn remains a distinct possibility.

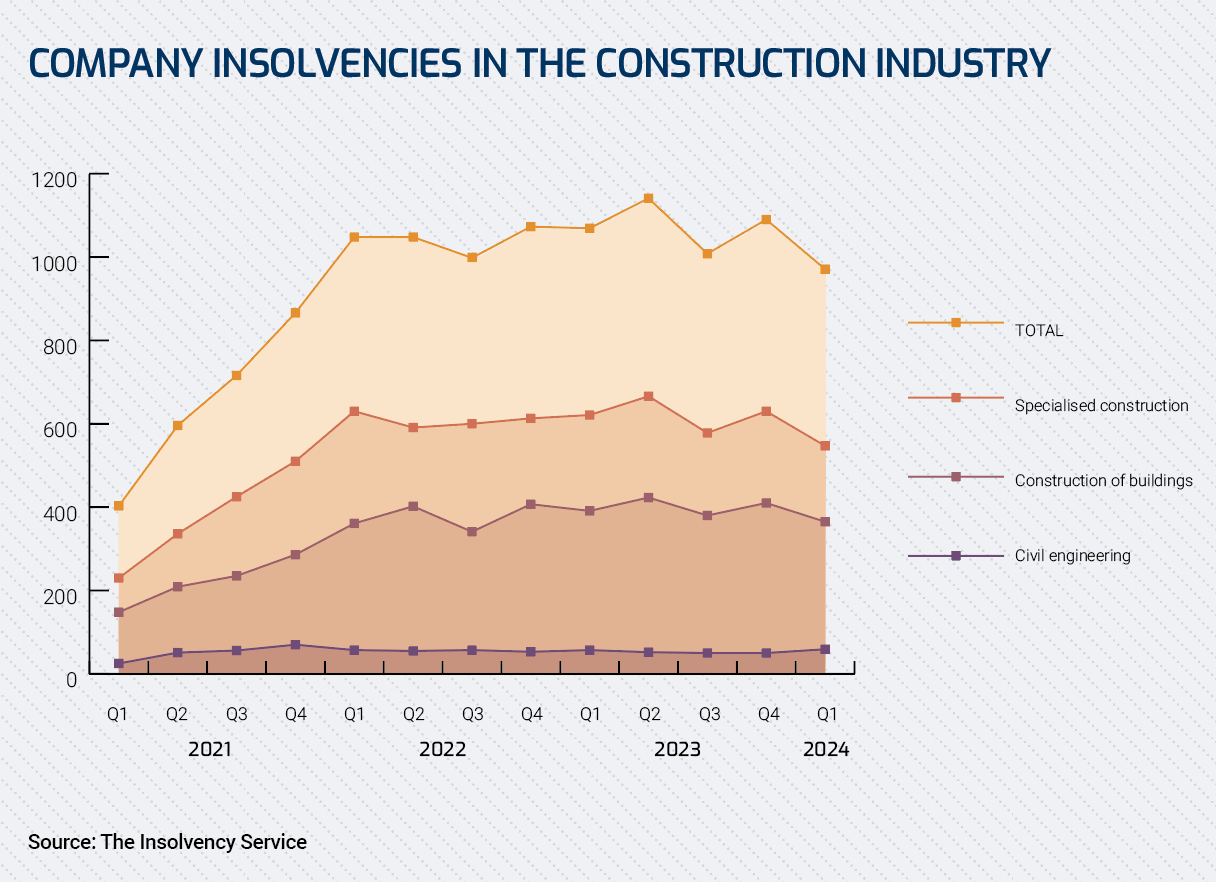

Insolvencies

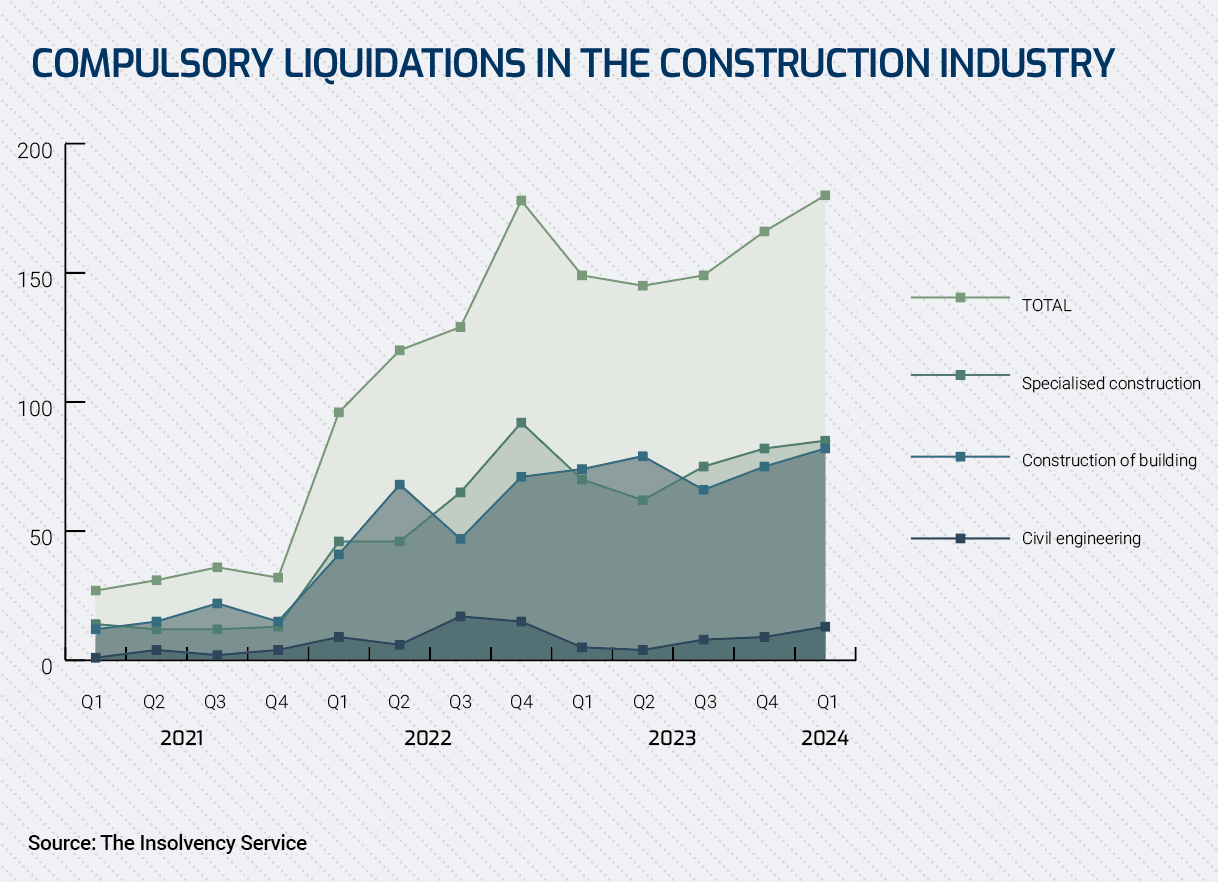

Wholesale reform of payment terms is needed to lift the construction industry out of its perennial position as the sector of the economy worst hit by insolvencies.

In the 12 months to May 2024, the Insolvency Service recorded 4,287 insolvencies in the construction sector. The next worst sector was retail with 3,811 cases of insolvency.

Fintan Wolohan, a managing associate in corporate and commercial business at consultants Womble Bond Dickinson, says: “The sector has perennially topped the charts for over a decade, reflecting an incredibly tough last few years for construction and the trail of hurdles the industry has had to overcome, including Brexit, the Covid-19 pandemic, the war in Ukraine, material and labour supply issues, steep rises in the cost of materials, wage inflation and increasingly extreme weather conditions – to name but a few."

There has been a 5% rise in insolvencies among construction companies with 1,600 going under. While the number of civil engineering firms becoming insolvent was static at 210, insolvencies among companies involved in the construction of residential and non-residential buildings leapt by 9% with 883 firms hit by insolvency. However it is the supply chain that is suffering the most.

Specialist contractors continue to bear the brunt of the continuing rise in insolvencies with 2,477 companies going under in this period. Insolvency Service data shows that 998 electrical, plumbing and other specialist installation contractors went bust in the 12 months to May 2024. This figure is marginally down on the preceding 12 months.

There was a 26% reduction in demolition contractors going under, with 51 insolvencies in the latest period, but finishing contractors continue to struggle. There was a 9% rise in the number of insolvencies in the latest period, when 885 specialist completion contractors failed.

These woes continued into the summer with well-known fit-out firms failing. Paramount D&B, a Welsh fit-out firm that turned over £30m a year, and historic façade contractor Charles Henshaw & Sons both filed for administration in July.

With a new government promising better times ahead (at least, for companies involved in residential construction) the need for reforms to address insolvency and sustain this workload has never been greater.

Kelly Boorman, national head of construction at the UK arm of consultants RSM, said: “With the new government’s commitment to 'get Britain building' for economic growth through the reintroduction of mandatory housing targets and planning reform, there needs to be focus on supporting distressed businesses and protecting labour.

“Government needs to reform payment terms and access to funding, especially for smaller and newer businesses, who would really benefit from continued improvements in payment practices. This would help to create fairer trading environments, with access to funding enabling innovation and efficiency, ensuring government delivers on its plans to accelerate housebuilding with 1.5m new homes over the next five years.”

A fundamental part of achieving that aim would look to be a stronger, more financially resilient supply chain with a significant reduction in insolvencies.

The Construction Rich List 2024

The number of families making their wealth from construction continues to rise with 21 people and their families appearing in the latest Sunday Times Rich List.

After rising 10 places in 2023, Lord Bamford and his family, owner of construction equipment giant JCB, are now among the country’s 20 richest families with their overall wealth surging to £7.65bn.

In contrast, the wealth of house-building magnate John Bloor, who owns the developer that bears his name as well as the Triumph motorcycle business, fell by £92m to below £3.4bn.

Many other house-builders increased their wealth ahead of a general election that was widely expected to buoy their industry. Former Redrow boss Steve Morgan, and the Gallagher family who own Abbey, both enter the latest top 200.

The Ainscough family, which controls Wain Homes, the McCarthy family – owners of retirement home builder Churchill – and David Wilson and his family all move up the table. Lower down, Michael Shanly and Andy Hill, who both own house-builders that bear their name, re-enter the list of the UK’s 350th richest families as does Emma Hindle, owner of Lancet Homes.

Contracting families are less prevalent but a couple of well-known names are enjoying good fortunes.

The Murphy family entered the Rich List for the first time only last year but have risen six places to joint 172nd as their wealth increased by £19m to £950m.

The Shepherd family sold its traditional construction business a decade ago to focus on its well-known modular building business, Portakabin. Since then the Shepherds have grown a substantial modular contracting business, which expanded further last year with the acquisition of Shropshire-based modular contractor Darwin.

The Shepherd family’s wealth also increased last year, up £411m to £1.1bn, prompting a rise of 89 places on the Rich List.

However, the wealth of the Kirkland family, which owns contracting behemoth Bowmer & Kirkland, rose by only £10m, prompting a return to their 2022 ranking of 207th position, while Ray O’Rourke – ranked 345th a year ago – drops out of the list altogether.

Further down, the Caddick family re-enters the Rich List while John Kelly, of the eponymous civil engineering contractor MV Kelly, is a new entry in 335rd place.

But with the new Labour government promising to build 1.5 million new homes over the next five years and already axing a number of major (and much-anticipated) infrastructure projects, it will be the house-builders rather than the contractors on the Rich List who can look forward to the biggest increase in their net worth this coming year.

Got a story? Email news@theconstructionindex.co.uk