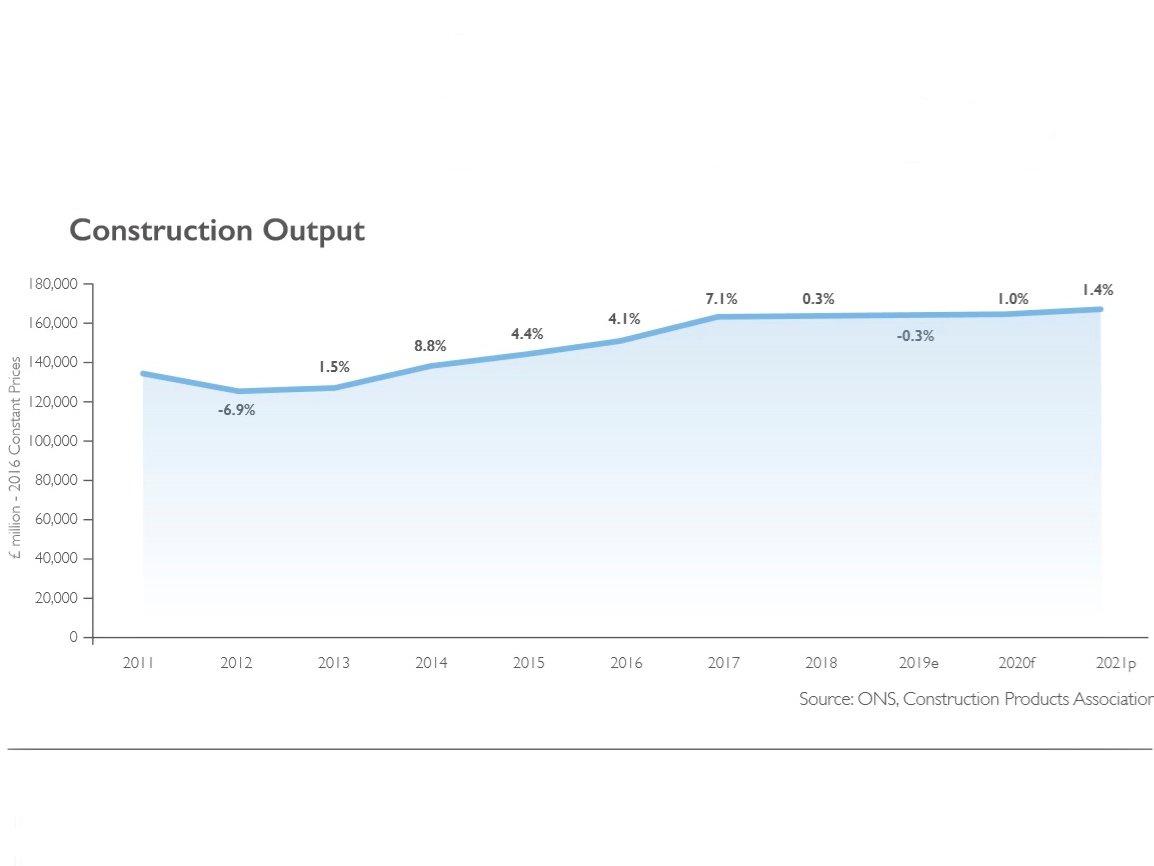

The Construction Products Association (CPA) Summer Forecast for 2019-2021 predicts a 0.3% decline in total construction output for 2019, in line with previous projections, but the forecasts for 2020 has been revised down to 1.0% from 1.4% just three months ago. The forecast for 2021 has been cut to 1.4% from 1.7% previously.

And these forecasts are based on the assumption that new prime minister Boris Johnson will pull off a smooth Brexit.

Meanwhile, on the retail side, the Builders Merchant Federation has downgraded its sales growth expectations for 2019 from 4.8% growth to 3.0%, blaming Brexit-related economic uncertainty.

The CPA Summer Forecast identifies the infrastructure sector as a main driver of growth and vital to the fortunes of the construction industry in the next few years. Total construction output would fall by 1.7% in 2019 and experience no growth up until 2021 without the delivery of major infrastructure projects, which have been put into further doubt given that Johnson has initiated a review of HS2 and is throwing his weight behind much cheaper schemes instead.

Major projects such as the Thames Tideway Tunnel and Hinkley Point C are expected to drive activity in the infrastructure sector as well as the new five-year regulatory periods in the water & sewerage, rail and roads sub-sectors. After almost a decade of austerity, local authority funding will also prove important to activity on roads, the CPA says, although the risk of delays to these projects makes the fortunes of the wider construction industry far from certain.

While the overall figure for construction output signals growth, there are variations across regions, sectors and sub-sectors. Levels of construction activity remain high in the Midlands, the Northwest and Yorkshire & Humber, while activity is set to decline in London, the Southeast and parts of the East of England.

On a sectoral basis, activity levels remain high in private and public housing, industrial warehouses and infrastructure. Subsectors such as commercial offices, commercial retail and industrial factories continue to endure falls in activity, however, mainly due to investor sentiment being impacted by the continued economic and political uncertainty surrounding Brexit, CPA predicts.

CPA economics director Noble Francis said: “Construction output in some key sectors has already been badly affected by Brexit uncertainty over the past 18 months and when you add in rising concern about government delivery of major infrastructure, it is a highly uncertain time for the construction industry. Activity on the ground, overall, still remains at a high level after rising by 28% between 2012 and 2017. However, output growth slowed to only 0.3% in 2018 and we forecast that construction output will fall by 0.3% in 2019 before growth of only 1.0% next year, even with a smooth Brexit and with government delivery of infrastructure projects.

“The fall in construction output during 2019 and 1.0% growth in 2020 masks the stark differences in regional and sectoral fortunes across the country. Infrastructure output is forecast to rise by 9.3% this year but this growth is highly dependent upon the delivery of the £4.2bn Thames Tideway Tunnel, the £19.6bn Hinkley Point C nuclear power station and the £56bn HS2 high-speed rail project.

“Private housing is the largest construction sector, worth £36bn in 2018, and it has been the key driver of industry growth over the past five years. Activity in the sector is currently slowing and private housing starts are forecast to fall by 2.0% this year before growth of 1.0% in 2020. The sharpest falls in new housing demand are occurring in London and the Southeast, particularly for prime residential flats. However, these falls are currently being partially offset by house building growth in the Northwest, Yorkshire and the Midlands, buoyed by Help to Buy. In these areas, a lack of key skills remains a key issue.”

He continued: “Construction output in commercial, the second largest construction sector, is worth £29bn in 2018. Commercial output fell by 6.4% last year and we forecast it will fall by 6.9% in 2019 and a further 4.7% in 2020 due to the impact of Brexit uncertainty on the offices sub-sector, in particular investment in new offices towers in London, as well the impact of continued shift of consumer spending online and its adverse impacts on new investment in retail construction.

“Overall, especially given the current high level of uncertainty, it is essential that government commits to better delivery of the major infrastructure projects that it says are essential for the country. Only then will construction provide a boost to UK economic growth and give firms the confidence to invest in vital capacity and skills as well as modern methods of construction such as digitalisation and offsite manufacturing.”

Got a story? Email news@theconstructionindex.co.uk