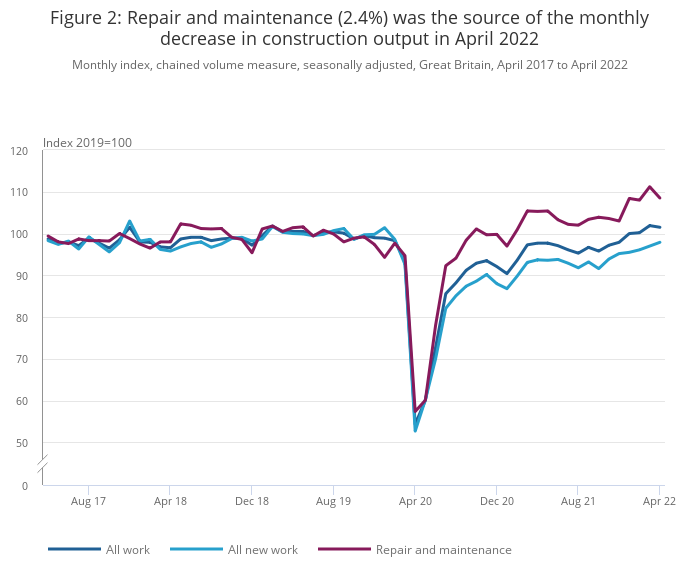

New work was up slightly in April, by 0.9%, but there was a 2.4% dip in repair and maintenance, attributed to a levelling out in activity after the spike in repair work after February’s storms.

However, the latest numbers from the Office for National Statistics (ONS) come with a health warning:

“Estimates for April 2022 are subject to more uncertainty than usual because of challenges we have faced with data collection,” ONS said. “This has led to lower response rates than those seen before the coronavirus pandemic.”

The main contributors to April’s decline in output were private housing repair & maintenance, and private commercial new work, which decreased by 6.5% and 3.8%, respectively.

Despite the monthly fall, the level of construction output in April 2022 was 3.3% (£481m) above the February 2020 pre-coronavirus level; new work was 0.7% (£68m) below, while repair & maintenance work was 11.0% (£549m) above.

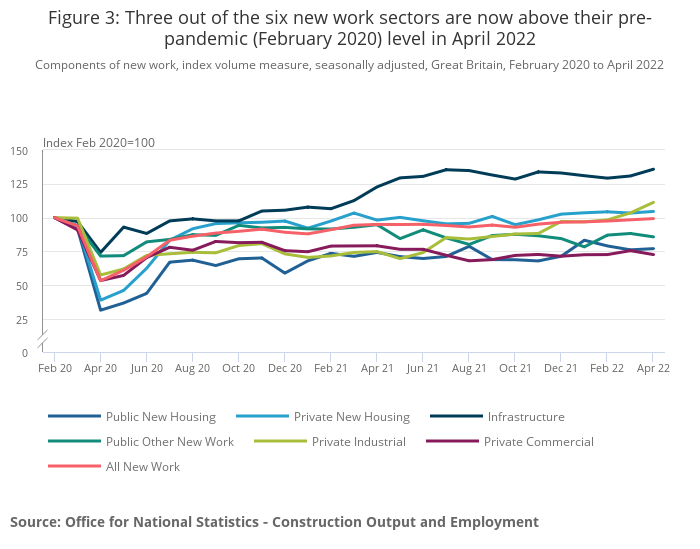

Since the falls in output at the start of the coronavirus pandemic, recovery has been mixed, with infrastructure 35.6% (£669m) above and private commercial 27.2% (£676m) below their respective February 2020 levels in April 2022.

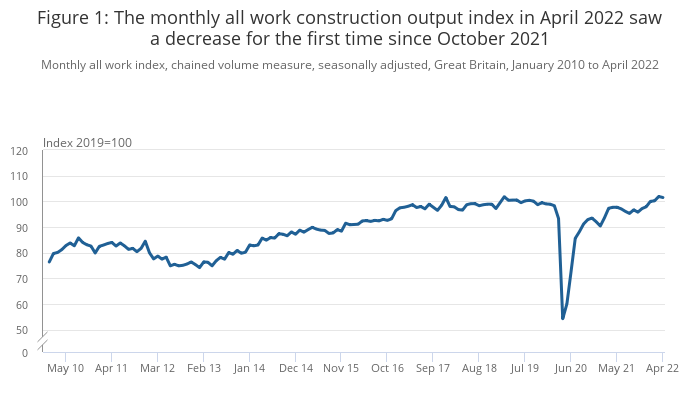

Despite April’s monthly decrease, construction output increased 2.9% in the three months to April 2022; this is the sixth consecutive growth in the three-month on three-month series, with increases seen in both new work and repair & maintenance (2.2% and 4.0%, respectively).

Gareth Belsham, director of the national property consultancy and surveyors Naismiths, commented: “Economic gravity and weakening business confidence have finally caught up with the construction industry. As the momentum of 2021 drains away, the slowdown has turned into a slide – with the sector posting its first monthly fall in output for seven months.

“But so far this is a cooling rather than a collapse. Private sector house-building continued to expand in April, climbing 1.1% compared to March and 6.5% compared to April 2021. There was a big jump in industrial sector construction too, up 7.6% on the month and a dizzying 48.7% on last April.

“On a quarterly basis, the picture is still positive. In the three months to the end of April, output grew by a respectable 2.9%, down from the 3.8% posted in the first quarter of the year. But no-one should be complacent. The pipeline of new work is starting to slow, with new orders falling by 2.6% in the first three months of the year compared to the final quarter of 2021.

“Once strong investment cases are being tested by soaring construction costs and nagging questions about what demand for the completed project will be like, and as a result increasing numbers of developers are pausing for thought before committing. While many construction firms still have reassuringly full order books for the coming months, the future beyond that is looking rapidly less rosy.”

However, Beard Construction finance director Fraser Johns was a little more optimistic. He said: “We should not be concerned by the small (0.4%) monthly decline in output volume. This is a re-balancing of the figures after they were temporarily inflated in March by a rise in demand for repair work after the winter storms.

“Instead, we should focus on the bigger-picture Q1 output, which shows a more encouraging 2.9% growth for the sector with April output more than 3% above pre-covid levels.

“That said, the drop in private commercial work to more than 25 per cent below pre-covid levels is a reminder that, for some areas of the sector, the recovery remains fragile.

“As the year unfolds and growing inflation carries on pushing up material prices, continued recovery will rely on open and honest conversations between main contractors, customers and the supply chain to ensure the cost plans for delivering schemes are both robust and realistic for all parties.”

Got a story? Email news@theconstructionindex.co.uk