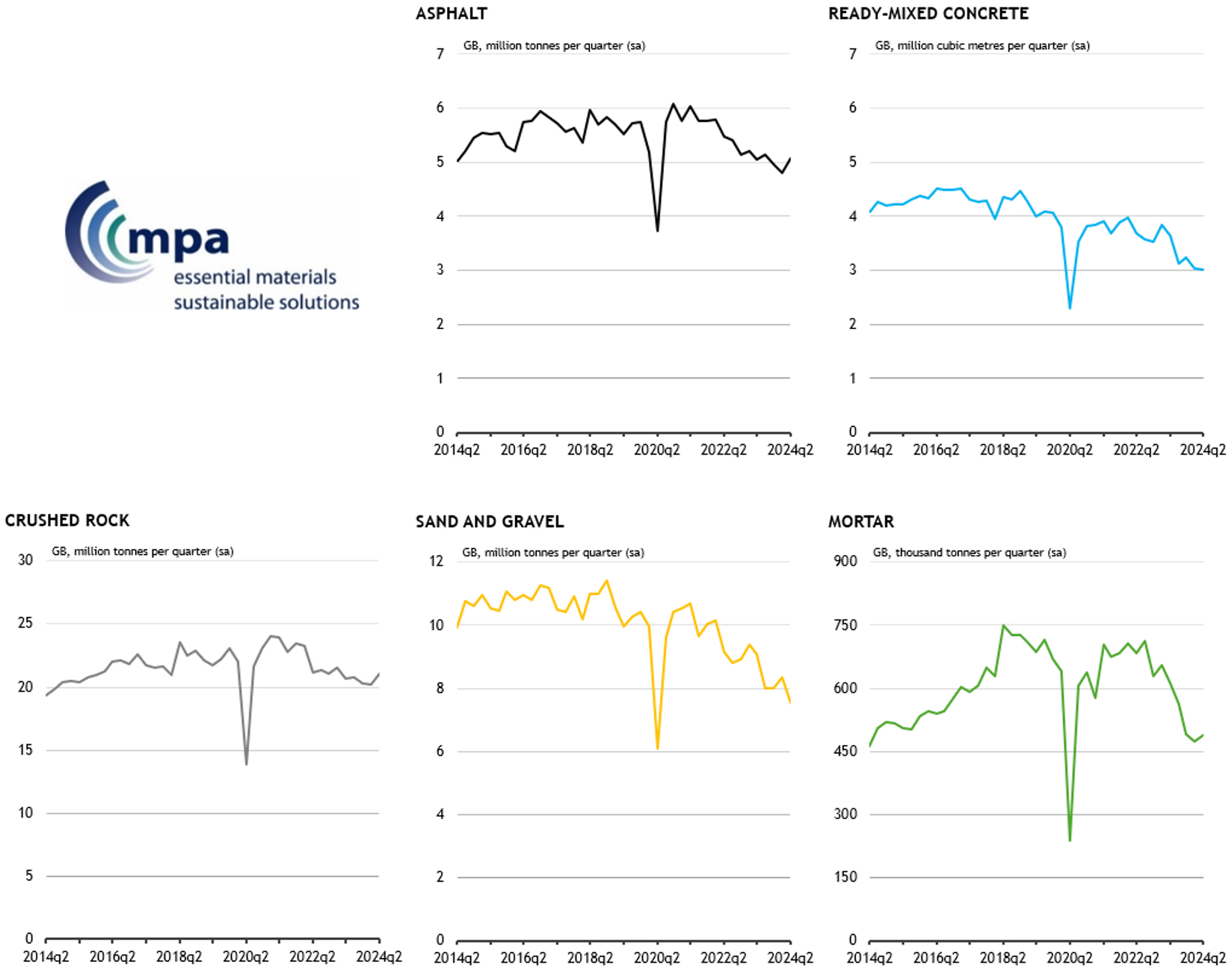

New figures from the Mineral Products Association (MPA) show a modest overall improvement in the sales of construction aggregates and asphalt in Great Britain for the second quarter of 2024.

However, concrete sales are still in the doldrums,

Asphalt volumes increased by 5.3% to 5.1 million tonnes in Q2 2024, crushed rock sales rose by 4% and mortar sales grew by 2.8% compared to the first three months of the year.

The seasonally adjusted figures reflect a stabilisation in key construction materials markets following a notably poor first quarter, which saw sales drop to their lowest levels in more than a decade. Infrastructure projects such as the A30 widening in Cornwall and A417 ‘missing link’ scheme in Gloucestershire have played a role in this improvement, the MPA said.

The construction industry supply chain landscape remains fragile, according to the MPA. For example, ready-mixed concrete sales dropped by a further 1.1% to 3 million cubic metres in Q2 2024, the lowest ready-mixed concrete sales volume in Britain since the 1960s. Sand & gravel sales fell by 10% in the second quarter.

The MPA said that these declines underscore the persisting weakness in Britain’s construction sector, particularly new housing and delivery of infrastructure projects. Slower than expected interest rate cuts by the Bank of England and high mortgage rates continue to dampen housebuilding activity, whilst key areas of infrastructure, such as roads, remain beset by high costs and planning delays.

Annual comparisons further underscore the mixed performance across different mineral products. While asphalt and crushed rock sales saw slight annual increases of 0.2% and 1.5% respectively in Q2 2024 compared to Q2 2023, ready-mixed concrete and sand & gravel were down 17.4% and 17.0% respectively. Mortar sales are also down by 20.3% year-on-year, despite a minor quarterly recovery.

MPA members have emphasised the importance of ongoing major infrastructure projects such as HS2 and Hinkley Point C in stabilising the market for mineral products. However, the lack of new flagship projects coupled with financial and planning challenges, continues to hinder a more robust recovery. The MPA's latest market forecast suggests that while 2024 will remain challenging, a more substantial recovery is not anticipated until 2025, starting from a low base.

MPA director of economic affairs Aurelie Delannoy said: “Investment uncertainty is hurting our sector and the broader construction supply chain. The latest cancellation of the Stonehenge tunnel and Arundel bypass schemes, following the previous cancellation of the northern leg of HS2, further erodes business confidence. Likewise, new government reviews on transport and the hospital building programme add to this uncertainty, turning any attempt to forecasting and business planning into parody. This worsens the already weak outlook for the industry.

“The chancellor must urgently address these issues by providing clear policies to reduce uncertainty and spur growth in line with the government’s ambitions. This includes improving delivery on critical infrastructure investment and upgrades, and ensuring that the planning system supports the domestic supply of minerals and mineral products, which is essential for the wider construction and economic recovery.”

Got a story? Email news@theconstructionindex.co.uk