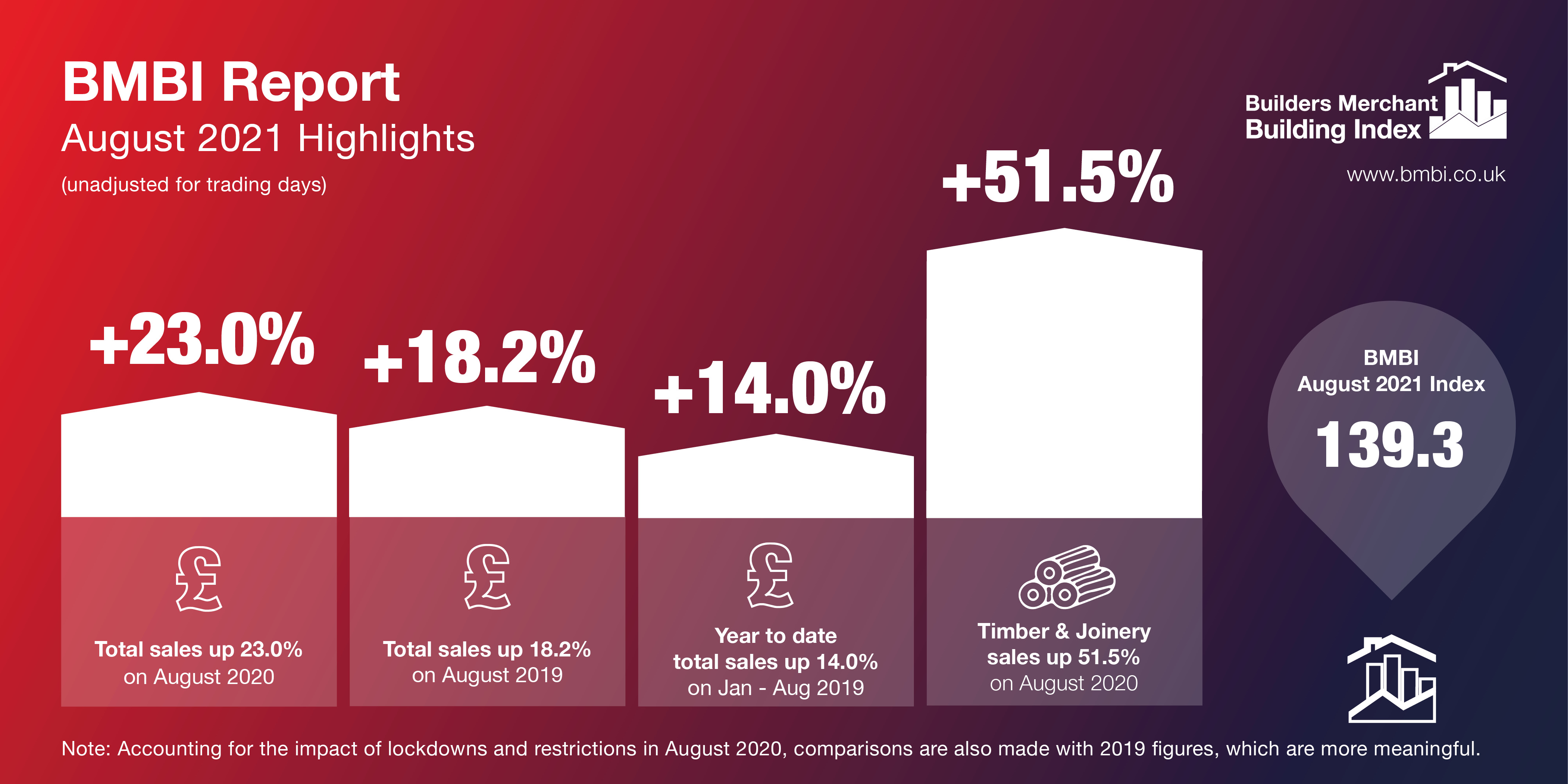

The latest report from the Builders Merchant Building Index (BMBI) reveals that the value of builders’ merchants’ sales in August 2021 was down nearly 8% on the previous month but 23.0% higher than August 2020 and 18.2% up on August 2019.

Timber & Joinery products was once again the fastest growing category, up 51.5% on the year, by value. Sales by volume are not measured, but given the increase in timber prices over the past year, are likely to be substantially lower than 50%.

Helped by one more trading day this year, 11 out of the 12 categories sold more in August 2021 compared to August 2020. Heavy Building Materials (+16.9%), Landscaping (+11.5%) and Kitchens & Bathrooms (+11.3%) put in a strong monthly performance. Workwear & Safetywear (-2.7%) was the only category to sell less over the period.

Average like-for-like daily sales in August 2021 were up 17.1% on the same month last year.

Compared to August 2019, before the pandemic affected business, total merchant value sales were up 18.2%, with the same number of trading days. Timber & Joinery sales were up 48.4% on August 2019 and Landscaping was up 29.7%). Heavy Building Materials (+10.1%), Services (+9.7%) and Kitchens & Bathrooms (+2.9%) also recorded higher sales compared to August 2019.

For the second month in a row, total merchant sales were down in August compared to July (-7.9%) with no difference in trading days. Only Workwear & Safetywear (+3.1%) sold more, while Plumbing, Heating & Electrical (-3.6%), Kitchens & Bathrooms (-6.5%), Heavy Building Materials (-7.2%) and Timber & Joinery Products (-8.6%) all sold less. Landscaping (-14.4%) was the weakest category month-on-month.

August’s BMBI index was 139.3, helped by strong performances from Timber & Joinery Products (182.6) and Landscaping (175.3). Seven other categories exceeded 100, including Heavy Building Materials (127.0), Ironmongery (120.2) and Kitchens & Bathrooms (118.3).

Mike Rigby, chief executive of MRA Research, which produces the report, said: “After a bumper year, sales began to ease over the summer. With all Covid restrictions removed in July, I expect a combination of exhausted people trying to grab a summer break and the continuing impact of material shortages and supply chain problems contributed to slowing sales. There are murmurs of material shortages easing but with no significant lessening of demand it will take time to shorten current long lead times for many products and solve the complicated supply chain problems.”

Emile van der Ryst, senior client insight manager at GfK Retail & Technology UK, which collects the point-of-sale data, added: “The exceptional growth seen against both 2019 and 2020 continues ahead, but we’re seeing the first stages of a pressurised market starting to ease off. Merchants have done well to manage supply chain challenges and continue to reap the rewards of this. Growth should continue to slow down in the coming months, especially with the stamp duty holiday coming to an end and some of the other wider UK economic challenges coming to the fore.”

Got a story? Email news@theconstructionindex.co.uk